{kind=link}

Ceri Breeze/iStock Editorial via Getty Images

Operationally at least, it really hasn’t been an easy couple of years for InterContinental Hotels Group (IHG). I mean, it’s not often in the investing world that poor results are solely down to misfortune, but with COVID there isn’t really much else you can say. Shareholders have just had to accept not only the outsized initial impact on the lodging industry, but also the fact that it will be one of the last to fully recover.

Unfortunately, events of the past couple of years have weighed on what I think is a fundamentally sound “quality growth” story. IHG’s business has evolved these past two decades to the point where it is now basically a pure manager/franchisor, bringing it into line with large-cap peers like Marriott International (MAR). While that’s not the be-all and end-all, the asset-light model does result in the firm throwing off a lot of cash and generally finding growth easy to fund.

Data by YCharts

Data by YCharts

As per above, the shares have long since recovered to pre-COVID levels in anticipation of the eventual industry-wide recovery. They aren’t obviously cheap, then, and there’s definitely some more near-term uncertainty on the horizon due to the Russia/Ukraine war. Still, this stock deserves a premium valuation on account of its underlying business, while I think its long-term growth prospects are also quite attractive. I’m opening with a ‘hold’ rating, largely due to the weakening short-term outlook.

An Asset Light Franchisor And Manager

IHG owns a bunch of hotel brands, the most significant of which are Holiday Inn (~25% of rooms), Holiday Inn Express (~36%), Crowne Plaza (~13%) and InterContinental (~8%). Its system has around 880,000 rooms in total across 6,000 hotels, and nearly all of them are tied to franchise (71%) or management agreements (28%) following asset disposals in the 2000s and 2010s.

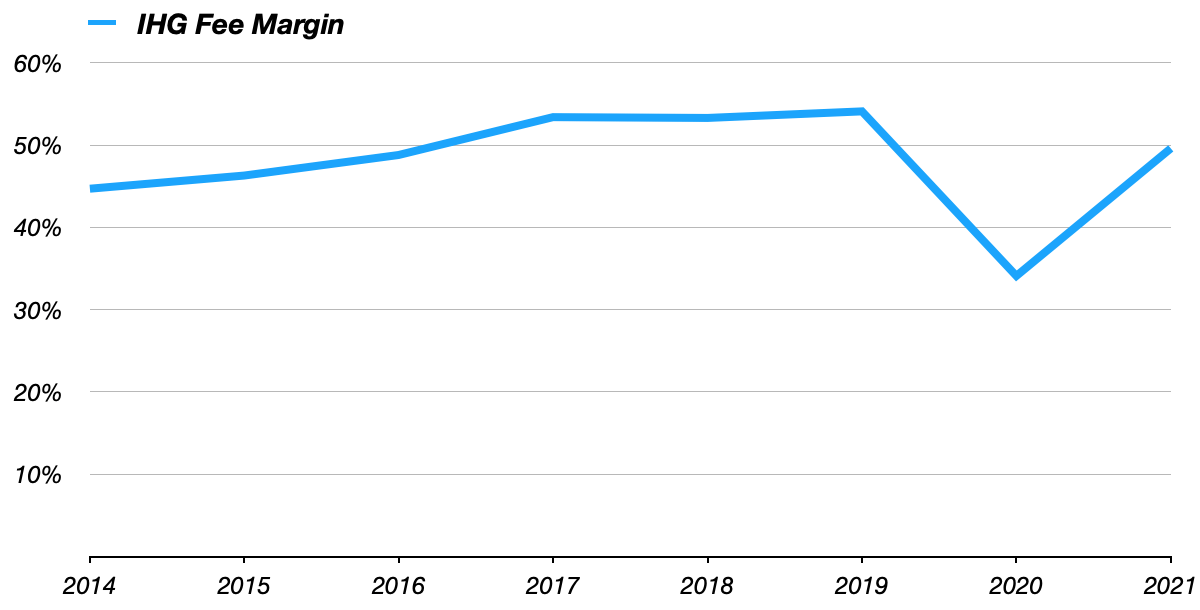

On the face of it, it’s not hard to see why investors would like that. IHG supplies its brands under license, and either gets a simple cut of room revenue (franchise), or a mix of a fixed cut of hotel revenue plus profit share (managed). Ultimately, around 80% of the group’s fee revenue is linked to hotel revenues. Most of the costs associated with actually running the hotels, not to mention the asset intensive business of dealing with physical hotel real estate, is left to its partners.

Source: IHG Annual Form 20-Fs

The upshot is that while IHG appears to post low revenue ($2.9bn last year versus “gross” system revenue of around $20bn), its margins and return on capital are very high, and that ultimately makes funding growth a lot easier, as well as allowing for plenty of cash to be returned to stockholders.

Slowly Moving On From COVID

The recovery from COVID has been a slow and uneven one, and realistically IHG and the wider lodging industry will be one of the last to fully recover. Indeed, domestic bookings in some markets are already back to 2019 occupancy and rate levels, especially bookings related to leisure. Business travel, international travel and group bookings remain weaker, though.

For 2021 as a whole, gross revenue in the IHG system was $19.4bn, up around 43% year-on-year but still down significantly on 2019 levels of ~$28bn. Likewise, global revenue per available room (“RevPar”) was up 46% year-on-year to $55.83, but still down ~30% on 2019 levels due to both lower occupancy and a lower average daily rate. Group-wide revenue was $2.91bn, down from $4.63bn in 2019, with operating profit of ~$500m also still below the $630m posted in 2019.

Within that, there is obviously a lot of volatility. Performance in the Americas (57% of rooms), for example, is currently relatively strong, with full-year RevPar ‘only’ down 20% on 2019 levels, helped by more domestic-oriented demand in the United States, particularly in leisure. Continuing sequential improvement in Q4 resulted in RevPar being down just mid-single digits on Q4 2019 levels, and December RevPar was actually up slightly on a two-year basis.

Elsewhere, the situation is more mixed. Europe, Middle East, Asia & Africa (“EMEAA”) (25% of rooms) remains weak, work improving, due to government restrictions and weak international travel demand, and EMEAA monthly RevPar remained 30% lower than 2019 levels in December. Greater China (18% of rooms) was more volatile, with RevPar falling in the back half of the year versus 2020 levels due to lockdowns.

TheOutlook

While the near-term will continue to be dominated by the recovery from COVID, IHG has also been thrown a curveball from the Russia/Ukraine war. In terms of the former, COVID-related demand destruction should continue to improve in 2022, particularly in Europe, with a full recovery by 2023 in terms of global industry-wide room stays.

In terms of the latter, IHG doesn’t have especially high direct exposure to Russia and Ukraine, but it will be sensitive to a global recession brought on by high energy prices. Indeed, economic growth estimates are being walked down worldwide right now, and that will inevitably weigh on the group’s RevPar.

I am much more bullish longer term. Net system growth did dip a bit last year, falling 0.6% to 880,327, but that was largely on the back of room disposals resulting from its reviews of the Crowne Plaza and Holiday Inn estates. Weak system growth in 2020 is also understandable considering the operating environment at the time.

Net system growth is guided much stronger across fiscal 2022 and 2023 (4-5% per annum), and I’m expecting at least low single-digits per annum thereafter, with the pipeline currently at around 270k rooms (40% of which is currently under construction).

The opportunity from growing emerging market wealth is immense, particularly in China. Indeed, China’s export-led economic model means its currency is artificially low right now, and while that makes inbound tourism relatively cheap, it means outbound tourism is more expensive. Eventually that will reverse, and that should prove a nice tailwind for international travel.

I also like the fact that management is beefing up its luxury estate, acquiring/introducing brands like Kimpton, Six Senses and Regent, with its share of the pipeline at around 20% (versus a low-teens share of the current estate). Luxury will naturally benefit from growing global (and emerging market) wealth, as luxury spending in general tends to grab an even higher share of growing disposable income. It should also be more immune to pressure from alternative service providers like Airbnb (ABNB).

Shares In The Fair Value Area

IHG ADRs have long since recovered to pre-COVID levels in anticipation of the recovery, and currently change hands in the $66 area in New York trading. While a full profit recovery is probably only a 2023 story, I do think IHG can go on to post long-term annualized free cash flow growth in the high single-digit area – with that coming from both RevPar and net system growth. Discounting that back to the present gives me a fair value in the $65 area, broadly where the shares are now. Hold.