{kind=link}

PATA’s new mid-year revision of Asia Pacific 2021-2023 Visitor Forecasts suggests a tough 2021, but with a rebound afterward, albeit in a very uneven manner.

The latest forecast is based on the latest data and information at its base, amid the extreme volatility in the travel and tourism sector caused by the Covid-19 pandemic and the resulting containment policies and measures to prevent its further spread.

The original PATA Asia Pacific Visitor Forecasts 2021-2023 report provided forecasts for that period using estimated baseline data for 2020, albeit on the most recent data for each of the 39 Asia-Pacific travel destinations. In the past few months, however, not only new data but also a number of other factors have surfaced that led to this scheduled review of the forecasts in light of these new developments.

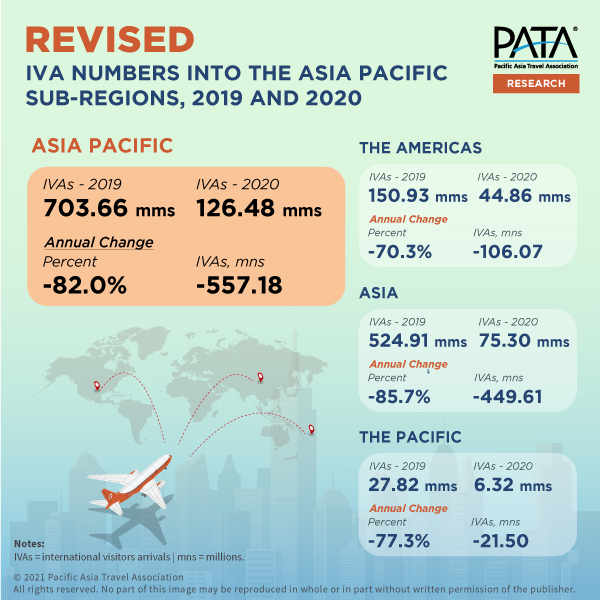

Across all 39 Asia-Pacific destinations, the difference between the estimates used in the original forecasts and those with the most recently published official arrival data was a positive plus of 3.8 percent. From an initial forecast of 121.843 million international visitor arrivals (IVA) in the original series in 2020, the actual values can now be updated to 126.475 million.

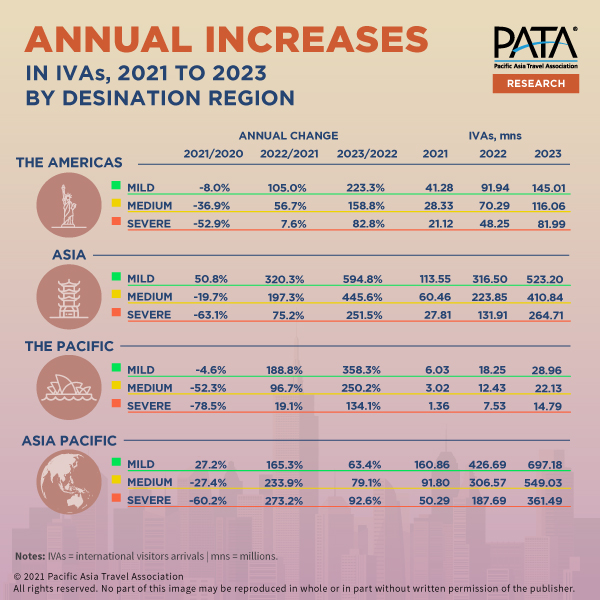

However, rates of contraction and loss of arrivals remain severe, with a total of more than 577 million foreign arrivals declining between 2019 and 2020. Unfortunately, these losses will continue through 2021 for most sub-regions in all scenarios. Asia is an exception, for which positive annual growth of almost 51 percent compared to the previous year is forecast in the mild scenario.

It is expected that this unique result will bring the overall position in the Asia-Pacific region to an annual growth of a little more than 27 percent between 2020 and 2021, but only in the mild scenario. All other positions remain negative during this period.

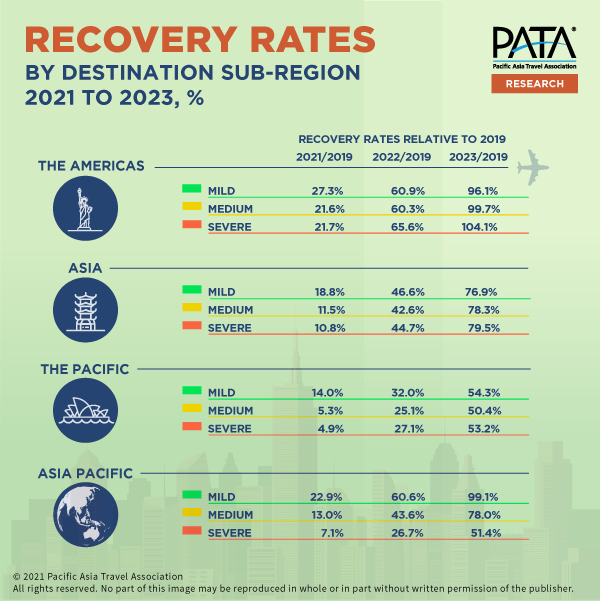

The good news, however, is that 2022 looks promising, with annual increases across the board ranging from gains of 105-320 percent in the mild scenario to 8-75 percent even in the severe scenario. However, it is important not to be seduced by such large annual percentage increases, because despite these increases, the absolute volume of arrivals for IVAs in some scenarios remains well below the benchmark for 2019 even until 2023.

The expected results for 2021 averaged just 23 percent of the 2019 volume at best. In the course of 2022, this should increase to 27 to 61 percent depending on the scenario and between 51 and 99 percent by 2023 depending on the prevailing scenario.

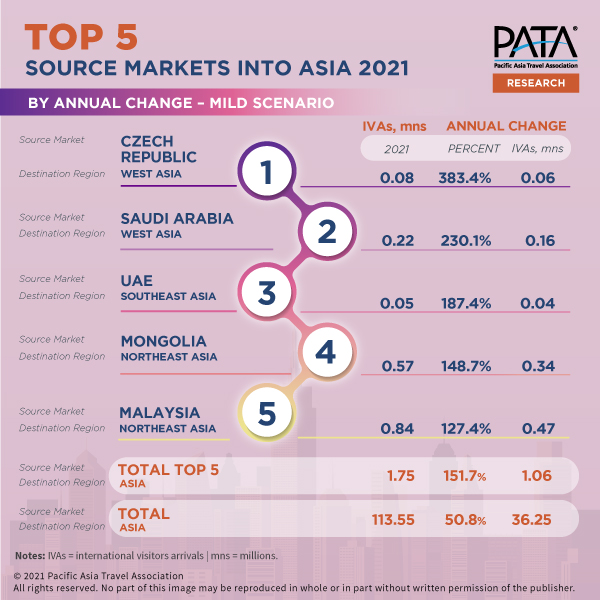

The mild-scenario increase in annual arrivals in Asia between 2020 and 2021 is expected to come from primarily Northeast Asian source markets, with the Russian Federation adding a gratifying number boost as well. Overall, this top 5 source market cluster is expected to bring an additional 29 million IVAs to Asia between 2020 and 2021, roughly 80 percent of the forecast increase in the region over that period.

Together with the increases in volume, Asia should see some significant annual percentage increases between 2020 and 2021. Although these increases are more than robust, the actual effects on the absolute volume of arrivals are minimal, but they strongly represent interest in the target region and are certainly worth a course over time to assess longer-term potentials.

Liz Ortiguera, CEO of PATA said, “We should postpone expectations of a return to the past and pay more attention to the source and target markets that are best preparing to fuel the recovery in the Asia Pacific region. The recovery of travel is driven by a complex number of factors, from different market policies for virus control and containment to local citizens’ views on vaccine acceptance.

“Success will be those who efficiently implement science-based pandemic control best practices in their home markets to restore both source market government and consumer confidence. In the travel industry, a due diligence approach to the delivery of services and products will support a more sustainable recovery.

“On the positive side, our forecast predicts a backlog of travel experiences in the Asia-Pacific region. Flexibility in marketing and providing new experiences to delight travelers with opening up the corridors will be critical. “